Interest-Bearing Account or Money Market Fund?

If you keep €100,000 of emergency savings in an interest-bearing account (cuenta remunerada) paying 2%, you are already losing €1,380 in the very first year compared with a money market fund paying 3%. That is not a subtle difference: these are real euros that either stay in your pocket or go down the tax drain.

The comparison that changes everything: real differences from day one

Imagine you have €100,000 for your emergency cushion. Let's see what happens with each option during the first year:

Interest-bearing account at 2%:

- You generate €2,000 gross

- The Spanish tax authority (Hacienda) takes €380 (19% tax)

- Your net gain: €1,620

- Final capital: €101,620

Money market fund at 3%:

- You generate €3,000, which is fully reinvested

- Hacienda takes nothing (tax deferral)

- Your reinvested gain: the full €3,000

- Final capital: €103,000

Difference in the first year: €1,380 in your favor. And that is just the beginning.

Tax deferral: your ally from minute one

With an interest-bearing account, Hacienda takes its share every year. With a money market fund, all of your money keeps working for you until you decide to redeem it. This advantage compounds dramatically over time.

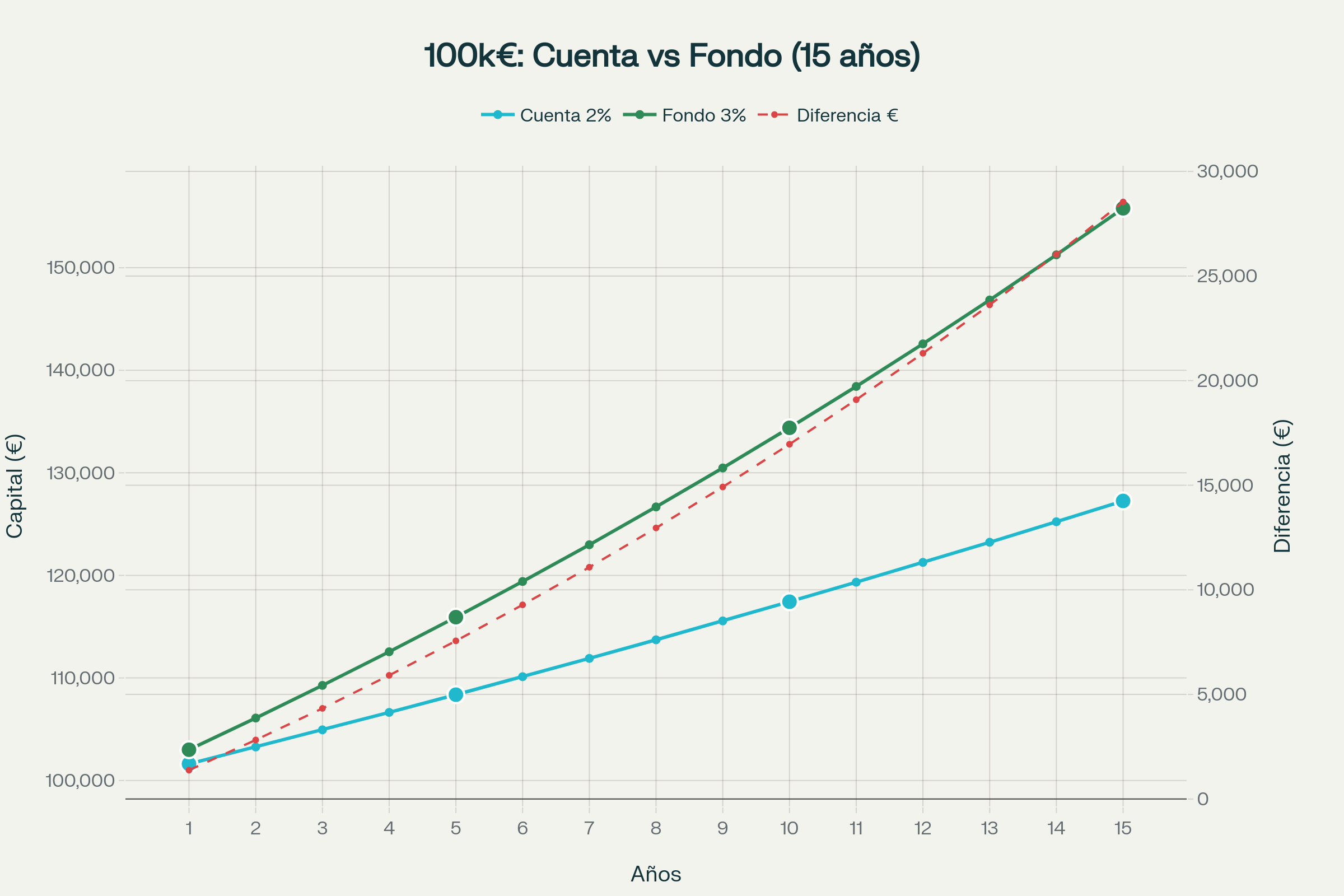

Evolution of an initial €100,000: significant differences from the very first year between an interest-bearing account and a money market fund

The chart shows how, starting with €100,000, the differences are evident from the first year and widen exponentially.

The evolution over time: why every year counts

| Year | Interest-Bearing Account | Money Market Fund | Difference | Advantage |

| 1 | €101,620 | €103,000 | €1,380 | 1.4% |

| 3 | €104,939 | €109,273 | €4,334 | 4.1% |

| 5 | €108,367 | €115,927 | €7,561 | 7.0% |

| 10 | €117,433 | €134,392 | €16,958 | 14.4% |

| 15 | €127,259 | €155,797 | €28,538 | 22.4% |

Note: Differences shown before the final taxation of the money market fund

The net comparison: what you actually keep

Even after deducting the final tax you would pay when redeeming the money market fund, the advantage is clear:

| Years | Interest-Bearing Account | Money Market Fund (net) | Difference | Total Advantage |

| 1 year | €101,620 | €102,430 | €810 | 0.8 % |

| 3 years | €104,939 | €107,511 | €2,572 | 2.5 % |

| 5 years | €108,367 | €112,901 | €4,534 | 4.2 % |

| 10 years | €117,433 | €127,857 | €10,424 | 8.9 % |

| 15 years | €127,259 | €145,195 | €17,937 | 14.1 % |

The phantom money working for you

Tax deferral is not just about postponing taxes. It means money that would have gone to Hacienda keeps generating returns:

- Year 1: an extra €570 working for you thanks to the deferral

- Year 3: an extra €1,762 generating returns for you

- Year 5: an extra €3,026 you would not have in an interest-bearing account

- Year 10: an extra €6,534 growing year after year

This "phantom money" turns into real euros thanks to uninterrupted compound interest.

The funds that capture this advantage

- La Française Trésorerie: With 1.43% YTD in 2025 and 3.82% in 2024, this fund shows how every euro that is not taxed gets automatically reinvested. On €100,000, we are talking about an extra €3,820 in 2024 that kept on growing.

- Groupama Trésorerie: It delivered 1.53% YTD in 2025 and 3.98% in 2024. Its track record of more than 30 years demonstrates consistency in harnessing tax deferral. On your capital, that is €3,980 that kept working without tax interruptions.

- BNP Euro Money Market: With 1.28% YTD in 2025 and 3.53% in 2024, it offers the solidity of BNP Paribas. Even with this more conservative return, that is an extra €3,530 that was not lost to annual taxes.

Fund transfers: multiplying the advantages

Money market funds allow TAX-FREE fund transfers (traspasos) under Spanish tax law. This means you can:

- Shift toward fixed income when conditions change (extend duration, take on a bit more credit risk...)

- Rebalance without tax penalties

- Keep the deferral going for decades if you so choose

This flexibility is impossible with interest-bearing accounts, where you are taxed automatically every year.

So, to sum up, the main advantages:

✅ Higher returns: 3% versus the 2% of interest-bearing accounts

✅ Tax deferral: You pay no tax until you redeem, letting all of your money keep working

✅ Uninterrupted compound interest: Every reinvested euro generates more returns year after year

✅ Tax-free transfers: Switch to other funds without triggering tax, keeping the deferral going

✅ Timing flexibility: Decide when to pay tax depending on your personal tax situation

✅ Sufficient liquidity: Access to your money in 2-3 business days

✅ Professional management: Funds run by teams specializing in short-term fixed income

✅ Wealth optimization: With €100,000, you generate an extra €810 in the very first year

✅ Cumulative effect: The advantage multiplies: an extra €4,534 over 5 years, €10,424 over 10 years

✅ No complexity: Simple, conservative, yet tax-smart products

Conclusion: your money deserves to grow without brakes

Every euro that goes to Hacienda each year is a euro that stops compounding. With significant amounts like €100,000, this difference turns into thousands of real euros.

Money market funds don't just offer higher returns: they offer compound growth without tax interruptions. And when you work with sizeable capital, this advantage becomes real money that makes a difference.

Your emergency fund doesn't have to be a dormant account at 2%. It can be a smart growth tool at 3% with a built-in tax advantage.

🎁 BONUS GIFT

If money market funds at 3% already clearly beat interest-bearing accounts, imagine the possibilities with ultra-short-term funds. These products, with slightly longer duration but still highly liquid, have delivered even more attractive returns:

- Ostrum Credit Ultra Short: It has delivered 3.60% over the last 12 months. On your €100,000 investment, that represents an extra €1,600 compared with an interest-bearing account, while keeping all the tax-deferral advantages.

- Groupama Ultra Short Term Bond: With 3.33% over the last 12 months, it offers an excellent balance between returns and conservatism. That is an extra €1,330 a year over an interest-bearing account, all reinvested tax-free until redemption.

- Tikehau Short Duration: Slightly higher up the risk spectrum, but with 3.90% over the last 12 months. For investors looking to get the most out of their conservative liquidity, it represents an extra €1,900 a year.

The key: These funds maintain 2-4 day liquidity and, above all, the same tax deferral. The difference is that they invest in debt with slightly longer maturities (6-18 months vs 3-6 months for pure money market funds), which lets them capture higher returns while keeping a conservative profile.

With €100,000 in Ostrum Credit Ultra Short over 5 years, you would generate roughly an extra €6,000 compared with an interest-bearing account, all compounding without tax interruptions until you decide to redeem.

Keep learning

Shall we talk about your wealth?

If you would like us to help you manage your wealth with professional judgement, write to us. The first conversation involves no commitment.

Request your first meetingFondos desde Cero, the newsletter

Every Tuesday, one investment fund analysed from the ground up — in Spanish. Over 2,200 investors already read it on LinkedIn.

Subscribe free on LinkedInWe need this information to better understand your needs — it will take less than a minute.