PIAS in Spain: What It Is, Pros and When It Makes Sense

Welcome to an in-depth, no-nonsense analysis of the Individual Systematic Savings Plan, better known as the PIAS (Plan Individual de Ahorro Sistemático). In the world of financial advice, it is crucial to stay informed and alert about the products we choose for our investment portfolio.

Below we will peel back the layers of the PIAS, demystifying the promises and exposing the realities that might make you think twice before taking one out.

1️⃣ What is a PIAS and why does it sound so attractive?

The Individual Systematic Savings Plan (PIAS) is marketed as an attractive solution for those looking for a safe and profitable way to save for the future. It promises to be a versatile investment vehicle, combining the benefits of insurance with the potential returns of investment funds.

The idea is simple: you make regular contributions that are invested with the aim of growing over time. At first glance, the PIAS looks like a solid option resting on three main pillars:

- Apparent tax advantages: It is promoted as a product with tax benefits, especially when you withdraw the money as a life annuity, where the capital gains are supposedly exempt from tax.

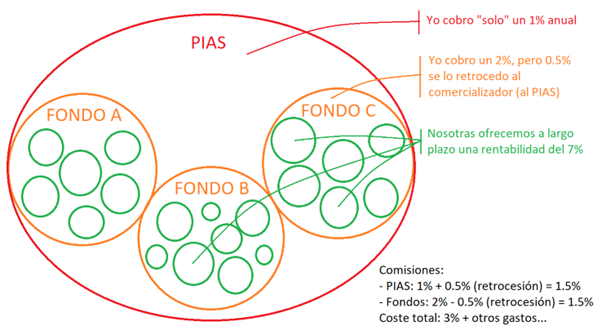

- Competitive costs: It is sold on the idea that management costs are low, around 1%, which in theory should leave more of your gains in your pocket.

- Professional fund management: The funds within a PIAS are run by professionals who, in theory, select the best investment options to maximize your return.

➖Tax advantages: a costly illusion?

The tax advantage of the PIAS is one of its most heavily promoted attractions. The argument is that, when redeemed as a life annuity, you benefit from a tax exemption on the capital gains generated.

This sounds ideal for anyone seeking tax efficiency in their retirement planning. However, this advantage is not as clear-cut as it seems:

- The tax reality: When you dig deeper, you find that the tax advantages of the PIAS are neither unique nor superior compared with other investment products.

- Misleading comparisons: The tax advantages of the PIAS are often compared unfavorably against less flexible or more expensive products, without giving a full picture of the alternatives available in the market.

➖Hidden costs: the reality behind the 1%

Although a 1% cost may look low, it does not tell the whole story. A PIAS can hide a far more complex and expensive cost structure:

- Layers of fees: What is rarely mentioned are the multiple layers of fees that build up in the background. These can include management fees, performance fees, the fees of the underlying funds the PIAS invests in, and other hidden costs that can eat into your returns.

- Long-term impact: These fees may seem small at first, but over time they can have a devastating impact on the growth of your investment.

2️⃣ Taking apart the promises of the PIAS

➖The false security of life annuities

The PIAS life annuity is promoted as a fortress of security for your future. However, this perception of safety can be misleading. While it offers a steady income during retirement, the terms are often not as favorable as they are painted.

Returns can be lower than with more direct market investments, and the lack of flexibility can limit your ability to adapt to changes in the market or in your personal circumstances. Investing in a diversified portfolio of investment funds, for example, could offer higher returns and a level of liquidity that life annuities cannot match.

In addition, strategies such as the 4% rule for retirement withdrawals can provide a similar income stream with greater control over your capital.

➖Opacity and conflicts of interest

You are promised that expert professionals are selecting the best funds to maximize your return. The reality, however, is often more complicated and less transparent.

Fund selection can be biased toward the funds that pay higher retrocessions (inducements) to the manager or the insurance company. This means the focus may be on maximizing their income, not yours.

The lack of transparency in fund selection and in the cost structure can leave investors in the dark about where their money really is and how it is being managed.

➖Questionable sales practices

Some PIAS distributors use sales tactics reminiscent of multi-level marketing schemes. These methods emphasize recruiting more salespeople and earning sales commissions, rather than focusing on whether the product is suitable and beneficial for the client. This approach can lead to insufficient or biased information about the true costs and limitations of the PIAS.

In some cases, pressure is applied to make quick decisions based on incomplete or misleading information. This can result in long-term financial commitments that are not in the client's best interest.

In addition, distributors sometimes use marketing tactics that present the PIAS as the only path to financial security, without mentioning its drawbacks or viable alternatives.

3️⃣ Why think twice before taking out a PIAS?

➖Misleading tax treatment:

Don't be dazzled by the tax advantage of the PIAS alone. Although it appears to offer favorable treatment, it is crucial to understand that these advantages are not exclusive to this product.

Many other investment vehicles offer similar or even better tax benefits, especially when considered as part of comprehensive financial planning.

A product's tax treatment should not be the only deciding factor; it should be weighed against other factors, such as flexibility, costs and expected returns.

➖High and hidden costs:

PIAS cost structures can be deceptively complex.

Beyond the explicit fees, there are hidden layers that can significantly erode your savings over time. These additional costs often stem from the fees of the underlying funds and other administrative charges.

It is essential to understand all the associated costs before committing, since even a small difference in fees can have a big impact on your investment's long-term performance.

➖Questionable returns:

The PIAS promises attractive returns through professional management, but the reality can be different. Returns depend on the fund selection and the manager's investment strategy, which may not always be aligned with your best interests.

Moreover, past performance is no assurance of future results, and the combination of high costs and an unclear strategy can erode the actual return you receive.

➖More transparent and flexible alternatives:

The market offers many options that may be better suited to your financial goals. These alternatives often provide greater cost transparency, clear investment strategies and the flexibility needed to adapt to your changing needs.

Exploring these options and comparing them with the PIAS will allow you to make a better-informed decision, one that matches your investment and tax-planning expectations.

4️⃣ Your financial strategy deserves more

A product like the PIAS can sound tempting with its promises of security and tax advantages, but it is essential to do your research and consider all the alternatives before making a decision. Not every product is right for every investor, and what works for one may not be best for another.

Remember that every financial situation is unique, and what works for one person may not be ideal for another. A financial adviser can help you understand the complexities of different investment products, including the PIAS, and find the path that best fits your needs and goals.

Keep learning

Shall we talk about your wealth?

If you would like us to help you manage your wealth with professional judgement, write to us. The first conversation involves no commitment.

Request your first meetingFondos desde Cero, the newsletter

Every Tuesday, one investment fund analysed from the ground up — in Spanish. Over 2,200 investors already read it on LinkedIn.

Subscribe free on LinkedInWe need this information to better understand your needs — it will take less than a minute.