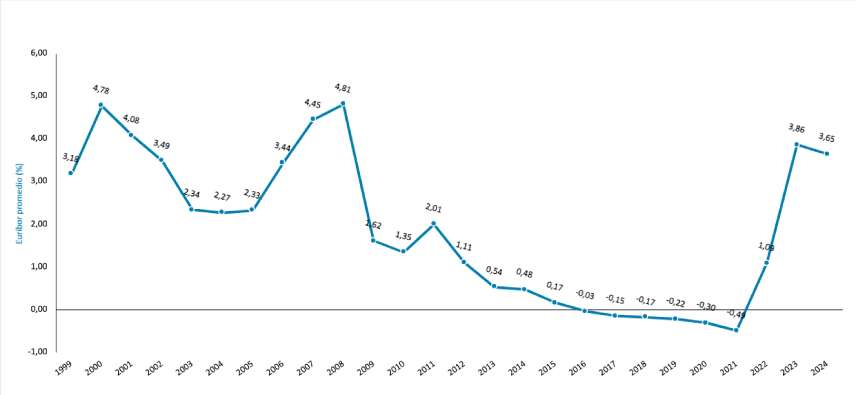

What is the Euribor? Its climb to 5%

The Euribor (Euro Interbank Offered Rate) is the interest rate at which the main European banks lend money to each other. In other words, it is the price a bank pays when it borrows money in euros from another bank.

This index is calculated daily and serves as the reference rate for millions of mortgages and financial products across Europe. If you have a variable-rate mortgage, it is most likely linked to the Euribor.

What is it used for?

The Euribor is used as a reference to calculate the interest on financial products such as:

- Variable-rate mortgages.

- Personal loans.

- Bank deposits.

- Financial derivatives.

For example, if your mortgage is referenced to "Euribor + 1%", it means you will pay interest equal to the current value of the Euribor plus an additional 1% that the bank applies as its spread.

How is it calculated?

Every business day, a panel of European banks reports the interest rate at which they would be willing to lend money to other banks. From this data, an average is calculated after discarding the most extreme values, and the result is published as the daily Euribor.

There are several types, depending on the term of the interbank loan:

- 1 week

- 1 month

- 3 months

- 6 months

- 12 months (the most widely used for mortgages)

Why does it rise or fall?

It rises or falls depending on economic factors, especially the European Central Bank's (ECB) decisions on interest rates.

- If the ECB raises rates, money becomes more expensive and the Euribor tends to rise.

- If the ECB cuts rates, money becomes cheaper and it tends to fall.

Other factors also play a role, such as inflation, confidence between banks and the economic outlook for the eurozone.

How does it affect your mortgage?

Suppose you took out a variable-rate mortgage with an annual review in January 2022, when the Euribor stood at -0.5%. If at the January 2025 review the Euribor is at +3%, your monthly payment will rise considerably.

This happens because your bank updates the interest rate you pay based on the Euribor in force at the time of the review.

Practical example:

- €150,000 mortgage over 25 years

- Interest rate: Euribor + 1%

- Euribor in 2022: -0.5% → you pay 0.5% total interest

- Euribor in 2025: 3% → you will pay 4% total interest

A change like this can mean hundreds of euros more per month.

Can I protect myself against rises?

Yes, there are some strategies to reduce the impact of a rise:

- Repay part of the mortgage early.

- Negotiate with your bank to review your interest rate.

- Switch your mortgage to another lender (subrogación) with better terms.

- Move from a variable-rate mortgage to a fixed-rate mortgage if you think rates will keep rising.

Conclusion: watching the Euribor means looking after your wallet

It is a technical index, but it has a very real impact on the finances of many households. Knowing how it works, what moves it and how it affects your mortgage allows you to make better-informed decisions.

🔍 If you have a variable-rate mortgage, it pays to keep a close eye on how the Euribor evolves and consider alternatives if the rises become a problem.

Shall we talk about your wealth?

If you would like us to help you manage your wealth with professional judgement, write to us. The first conversation involves no commitment.

Request your first meetingFondos desde Cero, the newsletter

Every Tuesday, one investment fund analysed from the ground up — in Spanish. Over 2,200 investors already read it on LinkedIn.

Subscribe free on LinkedInWe need this information to better understand your needs — it will take less than a minute.