Duration is a measure of a bond's interest rate risk that takes into account the bond's maturity, yield, coupon and call features. These many factors are combined into a single number that measures how sensitive a bond's value is to changes in interest rates.

Types of duration

There are two types of duration:

- Plain duration (or Macaulay duration) is the weighted average of the maturities of the bond's cash flows, weighted by the present value of each of those flows. It is expressed in years or as an abstract figure, and what it reflects is the relative change in price in response to relative changes in the yield to maturity (YTM). This concept was developed by Frederick Macaulay in 1938, hence its name.

- Modified duration (or Hicks duration) is the ratio of the Macaulay duration to one plus the asset's YTM, so it builds on the Macaulay concept. This measure reflects relative changes in price in response to absolute changes in the YTM and is expressed in years or as a percentage. In this case, it was the economist John Hicks who developed this mathematical relationship in 1939.

It allows you to calculate how long it takes an investor to recover a bond's price through the bond's total cash flows. It also makes it possible to assess how sensitive the price of a bond or a fixed income portfolio is to changes or fluctuations in interest rates.

Because some types of duration measures are calculated in years, duration is sometimes confused with time to maturity. However, a bond's term is a linear measure of the years until the principal payment falls due and does not change with the interest rate environment. Duration, by contrast, is not linear and accelerates as the time to maturity shortens.

Generally, the longer a bond's duration, the more its value will fall if interest rates rise, because when interest rates go up, the bond's price falls, and vice versa. If an investor expects interest rates to fall while holding the bond, a bond with a longer duration could be appealing because its value would rise more than that of comparable bonds with shorter durations.

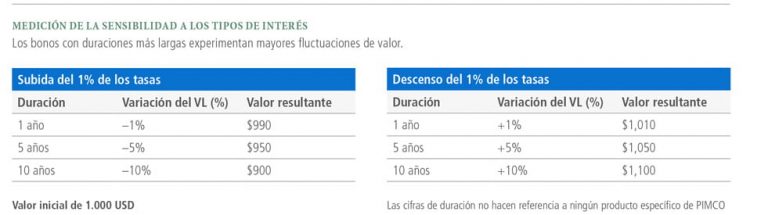

As the table below shows, the shorter a bond's duration, the less volatile it is likely to be. For example, a bond with a duration of one year would lose only 1% of its value if rates rose by 1%. A bond with a duration of 10 years, however, would lose 10% if rates rose by that same 1%. Conversely, if rates fall by 1%, bonds with longer durations would gain more, while those with shorter durations would gain less.

It is also worth mentioning that a bond's coupon rate, which is the nominal yield paid by a fixed income security, plays an important role in determining the bond's duration. So if we have two bonds that are otherwise identical but differ in their coupon, the bond with the higher coupon will pay back faster than the bond with the lower coupon or yield. As a result, duration and interest rate sensitivity decrease as the coupon rate rises.

Risk-averse investors, or those concerned about large swings in the capital value of their bond holdings, should consider a fixed income strategy with a very short duration. Investors who are more comfortable with these swings, or who are convinced that interest rates will fall, should consider longer durations.

Limitations of duration

Although duration can be an extremely useful analytical tool, it is not a complete measure of a bond's risk. For example, duration tells you nothing about a bond's credit quality or the fixed income strategy behind it. This can be particularly important for lower-rated securities (such as high yield bonds), which tend to react as much, if not more, to investor concerns about the stability of the issuing company as to changes in interest rates.

Another limitation of using duration to evaluate a fixed income strategy is that the average duration can change as the bonds within the portfolio mature and interest rates change. So the duration at the time of purchase may no longer be accurate once the portfolio's positions are in place. Interested investors should check the strategy's average duration regularly to avoid surprises, or invest in strategies that are actively managed to stay within an established average duration range.

Contact us

Shall we talk about your wealth?

If you would like us to help you manage your wealth with professional judgement, write to us. The first conversation involves no commitment.

Request your first meetingFondos desde Cero, the newsletter

Every Tuesday, one investment fund analysed from the ground up — in Spanish. Over 2,200 investors already read it on LinkedIn.

Subscribe free on LinkedInWe need this information to better understand your needs — it will take less than a minute.